Company Profile

PT Holcim Indonesia, Tbk. or we will simply

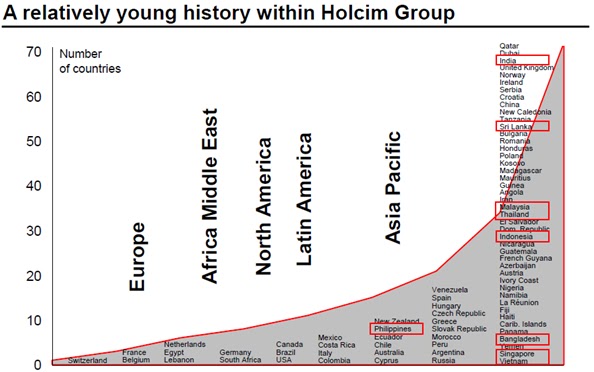

call Holcim Indonesia on this paper is one of subsidiaries that are holded by

Holcim, Ltd. which has its headquarter in Switzerland, Europe. Simply, this

graph will show us the position of Holcim Indonesia within the international

group.

In ASEAN, Holcim Indonesia has been holding

important role in cement industry. Don’t forget also that both Holcim Indonesia

and Holcim, Ltd. are mainly operating in cement industry in manufacturing

industry sector.

In Indonesia, Holcim Indonesia offers these

product lines:

1. Cement: 10 types of

cement are offered with roughly 7 milllions of tonnes of annual production.

2. Solusi Rumah: as a

new paradigm in cement business by providing houseowner abundant information of

building, starts from its design, until the details of costruction.

3. Aggregates: as the

industry of constructional mining—from Maloko, West Java to Jeladri, until East

Java.

4. Concrete: service of

constructional cement equipments provided by Holcim Indonesia.

5. Geocycle: the CSRs

of Holcim Indonesia while working with infrastructional businesses, it utilizes

the experiences of how to maintain the natural resources even in modern ways.

Holcim Indonesia

Financial Performance

On this section, we will start looking into

the critical content of the paper. In financial science, we have known exactly

that there are lots of tools to use in analyzing the financial performance of a

certain company but in this chapter we will merely limit our analysis among

these three sub section:

A.

Relationship between

IHSG (Jakarta Composite Index) and Holcim Indonesia: Return and Beta Analysis

These simple data

and graph were gotten from public reports between period we chose to analyze

the company:

·

Return Analysis

From the both charts and tables above, we can

directly take conclusion that both of them are showing positive trend in the

historical data. For the mean only, we might count better in Holcim Indonesia,

rather than the market. Thus, in Holcim Indonesia’s stocks, we might expect

more for the long run investment purposes.

However, the standard deviation and the

charts histogram showed us the debate that it is riskier to invest in Holcim

Indonesia with bigger and wider range of return than IHSG. The below chart even

shows us how in the period (ex-post analysis), risks to bear in order to get

returns have been bigger for Holcim Indonesia. Then, we should ask too: “How much is the dependance of Holcim

Indonesia to the volatility of market (IHSG)? Is the wide range in Holcim caused by its volatility to the IHSG?”

|

|

Holcim

Indonesia

|

IHSG

|

|

COVARIANCE

|

21.62096106

|

15.09545527

|

·

Beta Analysis (with IHSG)

Answer to the

question can be answered by doing beta (β) analysis for Holcim Indonesia as independent variable (Y) and IHSG as

its dependant variable (X) in Eviews.

|

Method: Least Squares

|

|

|

||

|

Date: 11/05/12 Time:

15:13

|

|

|

||

|

Sample (adjusted): 1 690

|

|

|

||

|

Included observations: 690 after adjustments

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C

|

0.000940

|

0.000812

|

1.157609

|

0.2474

|

|

X

|

0.052986

|

0.064464

|

0.821943

|

0.4114

|

|

|

|

|

|

|

|

|

|

|

|

|

|

R-squared

|

0.000981

|

Mean

dependent var

|

0.000984

|

|

|

Adjusted R-squared

|

-0.000471

|

S.D.

dependent var

|

0.021273

|

|

|

S.E. of regression

|

0.021278

|

Akaike

info criterion

|

-4.859384

|

|

|

Sum squared resid

|

0.311497

|

Schwarz

criterion

|

-4.846234

|

|

|

Log likelihood

|

1678.488

|

Hannan-Quinn

criter.

|

-4.854298

|

|

|

F-statistic

|

0.675590

|

Durbin-Watson

stat

|

2.119793

|

|

|

Prob(F-statistic)

|

0.411394

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Substituted Coefficients:

=========================

Y = 0.000939770978195 + 0.052986095495*X

First of all, we can

know the relationship between Holcim Indonesia and IHSG by testing them with

hypothesis testing:

1.

Hypothesis H0 : X = 0

H1 : X unequal 0

2.

T-critical = 1.647071412 (from Excel’s TINV formula)

3.

T-statistic

= 0.821943

(from Eviews table above)

4.

Thus, we reject H1 and conclude that IHSG as Beta (β) doesn’t significantly cause the

volatility of Holcim Indonesia stock returns.

Then, right after

figuring out that there is no significant relation between Holcim Indonesia and

IHSG, we can raise question: “So, what

influences the the risky movement of Holcim Indonesia stock return?”

Therefore, more fundamental analysis is required in the next comprehensions and

analysis point B and C.

B. Factors

that Influenced the Return Fluctuation of Holcim Indonesia Stock

After knowing that IHSG was not causing

Holcim Indonesia stock returns significantly, the major challenge we are having

is to determine and learn what are the risk we actually bear much from the

company. In order to analyze it, from the next page’s graph, we are going to

analyze the factors based on the “local period” trends that have been

distinguished or separated into 9 periods that we can simply judged from the

stock price graph, that must have finally constructed the stocks return. Every

major incident is hoped to be relevant enough to accomodate the appropriate

learning that we may have at the moment.

At the last part of this sub section of the

chapter, we will also look into account how the stock prices (reflected stock

returns) could be positively trending before concluding lessons we had from

them. I personally hope that these reports and comprehensions might give

broader view for all of the readers.

·

Period 1 (4 January – 26

April 2010): rapid and effective respose to the changing of external factors

during the year of 2009 was reavealed. Holcim, Ltd. was prepared for the market

slowdown after 2008 and in the beginning of 2009. Effective people development

programmes, debt and cost reductions were factors that influenced the high

expectation and rising values of the company. The 11.3% of sales rising was

surprisingly supported by 40% sales rises in concrete sales. Low inflation,

lower interest rate in the second half and strengthening Rupiah were supporting

factors that built positive sentiment for the strarting of 2010.

·

Period 2 (27 April – 21 May

2010): Execution of new cement plant in the eastern part of Java, near Tuban

which costed to around US$450 million was conducted. This attempt was done to

keep up the expected market growth. The new plant was hoped to further optimize

logistics costs and open up markets cost-efficiency in East Java, Kalimantan

and the eastern islands of Indonesia. Net sales and operating margin were also

revealed to grow in this period for Holcim Indonesia. However, heavy snowfall

and a weak economy unexpectedly limit construction activity in Europe and North

America. Even at this time, it was considered as difficult market environment

to grow, where Holcim exists in the regions too. At that time also, there was

an annual shareholders meeting that sounded not be that satisfied by the

devidend given by Holcim, but the meeting was held for the Holcim group,

Holcim, Ltd.

·

Period 3 (24 May – 7 December

2010): Stable volume development in all segments and increasing net sales –

operating EBITDA similar to the last year’s nine months when rapid recovery was

occured for the company, even as a whole. Demand of constructional materials

were all raising for emerging markets. Pressed prices was inevitable since low

fixed costs can be had but not for variable costs. There was reconstruction of

North America’s group’s interests. There was also special agreement with PT

Zurich Insurance Indonesia (ZII) to provide house insurance.

·

Period

4 (8 December 2010 – 14 March

2011): Holcim, Ltd. agreed to take plan to build new plants in France and

Switzerland for 8 locations to reach South Germany, Luxemburg, and the

Netherlands. However, by positive reports in ASEAN (even in Asia Pacific), the

group has planned to have additional constructional activities in Oceania in

the second half and is still confident that the Group will be successful in

securing its share of future growth in the emerging markets and that its lean

cost structures will enable it to benefit above average from a continuing

economic recovery in Europe and North America.

·

Period 5 (15 March 2011 – 20

July 2011): Dividends were distributed by withdrawing the 2010’s retainded

earnings with the reports of robust economic development in the emerging

markets. Inflation reduced cost pressure on raw materials and energy, as well

as strong Swiss franc, optimized the results to be significantly higher net

income.

·

Period 6 (21 July 2011 – 6

October 2011): Unexpectedly, Holcim Indonesia faced declining EBITDA, but report still showed higher net

income attributable to shareholders, the same factors happened in Latin

America, Asia Pacific, and Africa Middle East was down slightly compared to the

privious year because of downsiding movement off exchange rates among emerging

markets. Due to currency effects, consolidated net sales decreased by 7 percent

to CHF 10.1 billion and operating EBITDA declined by 19 percent to CHF 1.9

billion. The Group companies in Romania, Russia, Argentina, Thailand, Singapore

and Indonesia in particular positively influenced the result. At that moment,

Holcim still conducted the plant building in Brazil to increase its production

capacity.

·

Period 7 (7 October 2011 – 9

May 2012): Holcim 100 year’s anniversary evaluation of development and CSRs.

Continuable Bali projects added by two more innovative products by Holcim

Indonesia. Record sales was held and final Rp55/share dividend is announced.

Clear plant chedule of 1.7 million tonnes in Tuban factory. Domestic market

penetration raised and regional supply capability was proven to be run well.

For example, some Middle Sumatra projects were finished during the period by

using Holcim Indonesia’s group supplies.

·

Period 8 (10 May 2012 – 1

June 2012): Holcim provided CSRs to build 300 homes for low-income families in

Indonesia. The movement was also going in other emerging markets countries.

·

Period 9 (19 September 2012 –

19 October 2012): Indonesian

Environment Week 2012 or Pekan Lingkungan Indonesia (PLI) 2012 involves a

series of events held to promote World Environment Day, including the highlight

of the celebration at the State Palace on June 5. One of the key objectives of

PLI is to raise awareness of the environment. In order to achieve a broader

traction, future events will no longer focus on Jakarta and involve more

stakeholders in more regions. Higher operating EBITDA and higher cement volume,

better prices, also growth were supportive to all better margin for the Holcim

Indonesia with increasing shareholders’s value in increasing level. Moreover,

Holcim Indonesia attributed to lots of help for disables.

One thing that we might agree by seeing the occurances and the movement

of Holcim Indonesia’s stock prices is that the movements themselves somehow

were influenced by the investors’ behaviors. Thus, whether or not we use

‘proper’ behavioral analysis in finance, we might see some conditions that was

confirmed by the fluctuation of the stock prices (reflected the stocks

returns):

·

Holcim

Indonesia is a tough / aggresive company that wants to develop by so many

projects. Such a choice rather than being steadily improving may resulted in

next points.

·

Recall,

covariance (risk and return trade-off) of Holcim Indonesia is bigger than the

market.

·

The

behaviors of investors was obvously influenced by many foreign condition of

Holcim, Ltd. movements (can answer why it is significantly dependant with IHSG)

and currency risks accross countries, especially the condition of exchange

rates.

·

Investors

tend to be sensitive when:

o

The

company is taking projects (negatively)

o

The

company pays dividends (positively)

o

The

company almost finishes projects (positively)

o

The

exchange rates accross Holcim Ltd. changes (positively or negatively)

C. Analysis of Business Risks

Instead of merely concerning about how the stock prices fluctuated in

certain samples of period, as information seekers, we should develop broader

understanding about how the company has managed its businesses by take its

Financial Statements into account. One of most powerful tools to evaluate the

Financial Statements is when we discuss about the company’s Financial Ratios.

|

Summary of Financial Ratios

|

||||||

|

Holcim Indonesia, Tbk.

|

||||||

|

Category

|

2007

|

2008

|

2009

|

2010

|

2011

|

|

|

Liquidity Ratio

|

|

|

|

|

|

|

|

|

Current Ratio

|

1.332537

|

1.683279

|

1.269922

|

1.661888

|

1.465835

|

|

|

Quick Ratio

|

1.092369

|

1.345161

|

0.941218

|

1.293164

|

1.127042

|

|

|

Cash Ratio

|

0.641998

|

0.838355

|

0.370322

|

0.818776

|

0.708335

|

|

Efficiency Ratio

|

|

|

|

|

|

|

|

|

Inventory T/R

|

9.466971

|

7.586322

|

9.667207

|

7.423563

|

8.190659

|

|

|

Day's Sales in Inventory

|

38.5551

|

48.11291

|

37.75651

|

49.16777

|

44.56296

|

|

|

A/R T/R

|

7.604426

|

8.288687

|

8.955796

|

9.267229

|

10.672

|

|

|

Average Collection Period

|

47.99836

|

44.03593

|

40.75573

|

39.3861

|

34.20164

|

|

|

Total Asset Turnover

|

0.520918

|

0.625849

|

0.818112

|

0.571088

|

0.687089

|

|

|

Fixed Asset Turnover

|

0.658843

|

0.853004

|

1.083402

|

0.75282

|

0.911564

|

|

Leverage Ratio

|

|

|

|

|

|

|

|

|

Debt Ratio

|

0.68656

|

0.669325

|

0.543563

|

0.345996

|

0.31261

|

|

|

Debt to Equity Ratio

|

2.19234

|

2.024115

|

1.191347

|

0.529306

|

0.454779

|

|

|

Equity Ratio

|

0.313163

|

0.330675

|

0.456259

|

0.653679

|

0.68739

|

|

|

Equity Multiplier

|

3.193226

|

3.024115

|

2.191737

|

1.529803

|

1.454779

|

|

|

Times Interest Earned Ratio

|

2.584473

|

2.474226

|

3.915298

|

5.930663

|

8.967248

|

|

Profitability Ratio

|

|

|

|

|

|

|

|

|

Gross Profit Margin

|

0.336121

|

0.389377

|

0.378495

|

0.377372

|

0.378993

|

|

|

Operating Profit Margin

|

0.081016

|

0.106033

|

0.293052

|

0.231651

|

0.229361

|

|

|

Net Profit Margin

|

0.045117

|

0.058754

|

0.153486

|

0.139312

|

0.141356

|

|

|

Operating Income ROI

|

0.042203

|

0.066361

|

0.239749

|

0.132293

|

0.157591

|

|

|

ROA

|

0.023502

|

0.036771

|

0.125569

|

0.079559

|

0.097124

|

|

|

ROE

|

0.075048

|

0.111201

|

0.275214

|

0.12171

|

0.141294

|

Actually, it could be nice whenever we evaluate them all and that I

found out that it is really true that this company is an aggresive and can be

called as ‘risk-taker’ if it were an investor. The results are amazing from 5

consecutive years backward even though the passing global economic crisis. On

top of those discussions, these line might be said as the best ratios in order

to describe how the business risks of the company have been plotted.

In my opinion, there are lots of good things here. The most visible one

is the times interest earned ratio. It is obvious that the ratio is in line

with debt ratio too, but in the essence we can say that the significance of

getting operations done without any distraction of paying interests are greater

for this company (or in other word is ‘interest

independence’). One more good news for us is that those good ratios didn’t

reduce the ability of this company in generating profits. Fast recovery in 2009

still led Holcim Indonesia gets stable positive profitability. In financial

ratios point of views’ we can simply say that this company performed well, even

though such aggresive expectations may lead into high volatility of stocks

prices and returns movements. But, the good thing is that all of investments

(equity) to this company I am sure going to be positive in the long run.

Remember also, that beacuse this Holcim Indonesia has lots of

international investment and operations activities, we might be assured that

the portfolio systematic and unsystematic risks of the company are lower than

others commonly in Indonesia (recall: IHSG doesn’t significantly influence

Holcim Indonesia).

BCG Matrix Analysis

A.

Theoretical Review

At the moment we are

going to use BCG Matrix analysis in line with the intention with its founder,

Bruce Henderson for Boston Consulting Group in order to help people analyzing

business units or product lines within each company.

As shown above, BCG

matrix uses two-way axis: market / industry growth and relative market share

among the industry. Therefore, we have 4 quadrants built by the intersection

spaces among the two-way axis:

·

Cash Cows: refers to a company that can be judged to

have high relative market share but in slow industry growth. Thus, it looks

boring to be stagnantly in the one industry only. There can be opportunities of

getting profits in others.

·

Dogs: refers to company unfavorably to have. It has

significantly small relative market share, moreover in a slow growth industry.

·

Question Marks: refers to company that should have

more added-values to win the market which is in condition where fast industry

growth is experienced but in small relative market share.

·

Stars: refers to company that has bright future. It

is the most favorable where fast industry growth and big relative market share

are both experienced.

A.

BCG Matrix for

Holcim Indonesia

On this sub section,

in order to give us all rough but countable information about Holcim Indonesia,

I would like to distribute the results of my personal BCG Matrix Analysis for

the company into three layers:

·

Holcim, Ltd.

This is for Holcim Ltd. from my personal BCG Matrix. Based on next

page’s graph, it is obvious for us that this company has been able to define

all the time where the direction of infrastructional developments are

happening. Until now, Holcim, Ltd. is one of the biggest producers of cement in

the world. More over, not only about its size, but the profitability of this

company even could be managed time by time. Until it reached the time of slow

cement industry in developed countries to be refreshed in emerging countries.

·

Holcim Indonesia,

Tbk.

|

National Cement Industry Market Share

2010

|

|||

|

No.

|

Producers

|

Capacity

(million tonnes)

|

%

|

|

1

|

Semen

Gresik Group

|

20.2

|

37.0642202

|

|

2

|

Indocement

TP

|

18.6

|

34.1284404

|

|

3

|

Holcim

Indonesia

|

8.5

|

15.5963303

|

|

4

|

Semen

Bosowa

|

3.8

|

6.97247706

|

|

5

|

Semen

Andalas

|

1.6

|

2.93577982

|

|

6

|

Semen

Baturaja

|

1.3

|

2.3853211

|

|

7

|

Semen Kupang

|

0.5

|

0.91743119

|

|

|

TOTAL

|

54.5

|

100

|

|

(sumber: Asosiasi Semen Indonesia)

|

|||

|

Mean

|

7.785714286

|

||

|

Standard

Deviation

|

8.375246976

|

||

|

t-critical

|

2.015048372

|

||

|

t-test

|

-0.225643777

|

||

With CIA’s data of around 30%

budget is allocated to investments and previous page’s tables, we may know that

the growth for this market is high and even though we still reject the

hypothesis that Holcim Indonesia is significantly different at 95% confidence

level. This chart may give the BCG Matrix Analysis.

·

Holcim Indonesia’s

Business Units

o Cement:

o Solusi Rumah:

o Aggregates:

o Concrete:

For Cement and Aggregate, Holcim has been known as the specialist of

them among few producers in Indonesia as the keys to follow the rapid growing

of Indonesian ifrastructional development. Of course, by the enforcement of

governmental policies to develop it, any kind of industry / businesses related

to infrastructures will be growing too.

That’s why we can assume that for concrete and solusi rumah’s market growth are

promising, even though solusi rumah is still new and need to be supported,

while concrete is only reserve production projects of Holcim, since not in

every projects the equipments are always used.

Conclusion

Taking relationship

between company and market stock return and beta (β); elaboration more fundamental anlysis; and BCG

Matix Analysis into account are sufficient enough to highlight how certain

company has performed historically in order to get understanding how to invest

our company’s capitals. Unfortunately, right after figuring out that there is

no significant relation between Holcim Indonesia and IHSG, we should rely more

in simple fundamental analysis and BCG Matrix.

Then, after classifying Holcim Indonesia’s

ex-post analysis into 9 periods, some behaviors of investors were seen, even

though Holcim Indonesia is believed to give good long run profit. The movement of Holcim Indonesia’s stock

prices is that the movements themselves somehow were influenced by the

investors’ behaviors. Thus, whether or not we use ‘proper’ behavioral analysis

in finance, we might see some conditions that was confirmed by the fluctuation

of the stock prices (reflected the stocks returns):

·

Holcim

Indonesia is a tough / aggresive company that wants to develop by so many

projects. Such a choice rather than being steadily improving may resulted in

next points.

·

Recall,

covariance (risk and return trade-off) of Holcim Indonesia is bigger than the

market.

·

The behaviors

of investors was obvously influenced by many foreign condition of Holcim, Ltd.

movements (can answer why it is significantly dependant with IHSG) and currency

risks accross countries, especially the condition of exchange rates.

·

Investors

tend to be sensitive when:

o

The

company is taking projects (negatively)

o

The

company pays dividends (positively)

o

The

company almost finishes projects (positively)

o

The

exchange rates accross Holcim Ltd. changes (positively or negatively)

The most interesting ratio is the times interest earned ratio. It is

obvious that the ratio is in line with debt ratio too, but in the essence we

can say that the significance of getting operations done without any

distraction of paying interests are greater for this company (or in other word

is ‘interest independence’). One more

good news for us is that those good ratios didn’t reduce the ability of this

company to generate profits. Fast recovery in 2009 still led Holcim Indonesia

gets stable positive profitability. In financial ratios point of views’ we can

simply say that this company performed well, even though such aggresive

expectations may lead into high volatility of stocks prices and returns

movements. But, the good thing is that all of investments (equity) to this

company I am sure going to be positive in the long run.

Remember also, that beause this Holcim Indonesia has lots of

international investment and operations activities, we might be assured that

the portfolio systematic and unsystematic risks of the company are lower than

others commonly in Indonesia (recall: IHSG doesn’t significantly influence

Holcim Indonesia).

For the business units, Holcim Indonesia is

still one of the biggest producers in Indonesia, supported by 2 main business

units and 2 additional business units (concrete is to utilize equipment and

solusi rumah is to penetrate the growing market, while we might consider

geocycle as its CSRs, not the core products.

Thus, for all I am really satisfied by Holcim

Indonesia and I can take a lesson personally that this company is risky to be

invested only in short-term contract, but if it is in long run, I believe that

it is going to be better off, especially when the company has no signifficant

systematic risks in IHSG. Thus, it became a preferable choice of portfolio of

investment. God bless you all.

References

Adhy, Susilo. 2009. Analysis BCG

Matrik pada Suatu Perusahaan. [slam’s] son blog

Gujarati. Basic Econometrics.

Ross. Corporate

Finance Fundamentals

{kind=link}